- 销售与服务热线

- 180 8647 3890

汽车行业利润率,又下滑了

汽车行业利润率,又下滑了

从产销规模的稳步增长到能源结构的加速迭代,汽车行业正迎来结构性变革的关键期。然而,与行业规模扩张形成鲜明对比的是,盈利水平持续承压的困境——汽车行业利润率不仅低于下游工业企业平均水平,更处于历史相对低位。

规模增长但利润收缩,8月利润率创同期新低

整体来看,当下汽车行业呈现出鲜明的 “规模增长、利润收缩” 特征。

据乘联分会秘书长崔东树分享的数据,在汽车置换更新补贴等政策拉动下,2025年1-8月全国汽车生产总量达到2083万台,较去年同期增长11%,这带动了汽车行业收入的整体提升,1-8月,汽车行业收入达到68049亿元,较去年同期增长了8%。

图片来源:公众号“崔东树”

图片来源:公众号“崔东树”

不过聚焦盈利情况,压力却持续凸显,1-8月汽车行业利润总额为3035亿元,同比下降0.3%,行业利润率为4.5%,相对于下游工业企业利润率6%的平均水平,汽车行业利润率仍属于偏低水平。

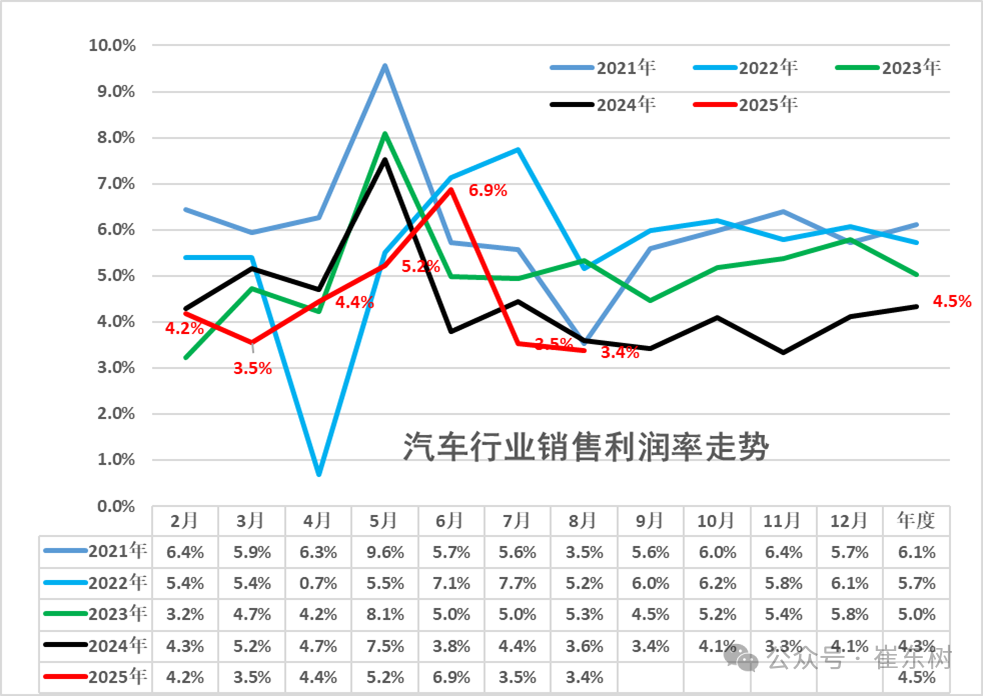

回顾近几年,汽车行业利润率整体呈现持续下滑态势。乘联分会数据显示,2021年汽车行业利润率为6.1%,2022年降至5.7%,2023年进一步下探至5%,2024年汽车行业销售利润率仅为4.3%,较历史正常水平大幅下降,成为行业盈利压力的集中体现。

尽管2025年1-8月4.5%的行业利润率好于2024年,但仍处历史次低位。且值得注意的是,2025年8月单月行业盈利状况进一步恶化。数据显示,8月汽车行业收入达到8856亿元,同比增7.5%,而利润仅298亿元,同比下滑10%,汽车行业利润率为3.4%,环比7月下降明显,相较去年8月的3.6%仍有下降,处于历年同期的利润历史低点。

崔东树指出,由于汽车行业产销基本持平、差距较小,可借用国家统计局产量数据测算单车经济指标。由此测算,1-8月汽车行业产业链的总体单车收入32.7万元(有产业链的重复计算),产业链单车利润1.5万元。

多重压力叠加,行业盈利陷入结构性困局

汽车行业利润率的持续下滑并非单一因素导致,而是成本刚性约束、市场竞争内卷、产业链分配失衡与宏观环境变化等多重压力交织作用的结果,形成了难以短期突破的结构性困局。

成本端的“双向挤压”构成了盈利下滑的基础诱因。在原材料领域,尽管大宗商品价格低位运行在一定程度上减轻了中下游行业的原料成本压力,但汽车产业链的核心部件成本压力并未得到有效缓解。作为新能源汽车核心成本的电池,其利润分配格局长期向上游倾斜,多数整车企业不具备电池生产能力,即便上游碳酸锂价格出现阶段性回落,成本红利也难以有效传导至整车环节,反而被电池生产企业截留。

数据显示,2025年1-8月,汽车行业成本总额增至59889亿元,同比增速达8.2%,超过收入增速。行业成本增速超过收入增速的差异,正是这种成本传导不畅的直接体现。同时,人工、研发、物流等刚性成本的持续上涨,进一步压缩了企业的利润缓冲空间,形成“上游成本难降、下游成本难控”的双向挤压态势。

市场竞争激烈成为利润率下滑的核心推手。自2023年以来,汽车行业的价格战已从新能源领域全面蔓延至燃油车市场,形成全品类、全价位的竞争红海。尽管2025年随着国家反内卷工作持续推进,价格战激烈程度已有多减弱,且对改善行业利润的促进效果已有所体现,但仍有待持续调整。

宏观经济与政策环境的“双重影响”进一步制约了盈利改善空间。从宏观层面看,PPI下行导致汽车产品定价面临压力,企业难以通过提价转移成本压力。从政策层面看,尽管新能源汽车补贴、置换更新等政策有效拉动了销量,但政策退坡预期下的企业抢装行为加剧了短期竞争压力,而“反内卷”政策虽已在钢铁等上游行业显现效果,但在汽车终端市场的传导仍需时间。此外,燃油车与新能源汽车的发展不平衡问题凸显,燃油车盈利下滑未能被新能源汽车的增长完全对冲,“油电转型”过程中的阵痛期仍在持续。

展望未来,汽车行业利润率的改善仍面临诸多挑战。新能源汽车渗透率的持续提升虽为行业带来长期机遇,但短期“以价换量”的竞争惯性难以快速扭转;上游成本压力的缓解需要产业链协同发力,而利润分配格局的重构更是一个长期过程。

崔东树直言,结合前几年的利润率下行趋势看,近期汽车行业利润下滑幅度仍较大,由于政策加持下的新能源价格优势明显,主流车企盈利压力仍将急剧增大。

不过,随着国家“反内卷”工作的深入推进、油电同权等政策的落地实施,以及企业在技术创新与成本控制上的持续努力,行业仍有望逐步摆脱“规模虚胖”与“利润微薄”的困境,实现利润率的稳步回升。

The profit margin of the automotive industry has declined again

From steady growth in production and sales scale to accelerated iteration of energy structure, the automotive industry is entering a critical period of structural transformation. However, in sharp contrast to the expansion of the industry scale, there is a dilemma of sustained pressure on profitability - the profit margin of the automotive industry is not only lower than the average level of downstream industrial enterprises, but also at a relatively low historical level.

Scale growth but profit contraction, August profit margin hits a new low for the same period

Overall, the current automotive industry exhibits distinct characteristics of scale growth and profit contraction.

According to data shared by Cui Dongshu, Secretary General of the China Association of Automobile Manufacturers, the total production of automobiles in China from January to August 2025 will reach 20.83 million units, an increase of 11% compared to the same period last year, driven by policies such as subsidies for automobile replacement and updates. This has led to an overall increase in the revenue of the automobile industry. From January to August, the revenue of the automobile industry reached 6804.9 billion yuan, an increase of 8% compared to the same period last year.

Photo source: official account Cui Dongshu Photo source: official account Cui Dongshu

However, focusing on profitability, the pressure continues to be prominent. The total profit of the automotive industry from January to August was 303.5 billion yuan, a year-on-year decrease of 0.3%, and the industry profit margin was 4.5%. Compared with the average profit margin of 6% for downstream industrial enterprises, the profit margin of the automotive industry is still relatively low.

Looking back at recent years, the overall profit margin of the automotive industry has shown a continuous downward trend. According to data from the China Association of Automobile Manufacturers, the profit margin of the automotive industry was 6.1% in 2021, dropping to 5.7% in 2022 and further dropping to 5% in 2023. In 2024, the sales profit margin of the automotive industry was only 4.3%, which is significantly lower than the historical normal level and has become a concentrated reflection of the industrys profit pressure.

Although the industry profit margin of 4.5% from January to August 2025 is better than in 2024, it is still at a historically low level. It is worth noting that the industrys monthly profitability will further deteriorate in August 2025. Data shows that in August, the revenue of the automotive industry reached 885.6 billion yuan, a year-on-year increase of 7.5%, while the profit was only 29.8 billion yuan, a year-on-year decrease of 10%. The profit margin of the automotive industry was 3.4%, a significant decrease compared to July last year, and still a decline from 3.6% in August last year, which is at a historical low point in profit for the same period in previous years.

Cui Dongshu pointed out that as the production and sales of the automotive industry are basically balanced and the gap is small, the production data of the National Bureau of Statistics can be used to calculate the economic indicators of bicycles. Based on this calculation, the overall bicycle revenue of the automotive industry chain from January to August was 327000 yuan (with double counting of the industry chain), and the bicycle profit of the industry chain was 15000 yuan.

Multiple pressures add up, causing the industrys profitability to fall into a structural predicament

The continuous decline in profit margins in the automotive industry is not caused by a single factor, but rather the result of multiple pressures such as rigid cost constraints, internal competition in the market, imbalanced distribution in the industry chain, and changes in the macro environment, which have formed a structural dilemma that is difficult to break through in the short term.

The two-way squeeze on the cost side constitutes the fundamental incentive for profit decline. In the field of raw materials, although the low prices of bulk commodities have to some extent alleviated the cost pressure of raw materials in the middle and downstream industries, the cost pressure of core components in the automotive industry chain has not been effectively alleviated. As the core cost of new energy vehicles, batteries have long tilted their profit distribution pattern towards the upstream. Most vehicle manufacturers do not have battery production capacity, and even if the price of lithium carbonate in the upstream temporarily falls, the cost dividend is difficult to effectively transmit to the vehicle link, and is instead intercepted by battery production companies.

Data shows that from January to August 2025, the total cost of the automotive industry increased to 598.89 billion yuan, with a year-on-year growth rate of 8.2%, exceeding the revenue growth rate. The difference between the growth rate of industry costs and the growth rate of revenue is a direct manifestation of the poor transmission of costs. At the same time, the continuous increase in rigid costs such as labor, research and development, and logistics has further compressed the profit buffer space of enterprises, forming a two-way squeezing trend of difficult to reduce upstream costs and difficult to control downstream costs.

The profit margin of the automotive industry has declined again

The fierce market competition has become the core driving force behind the decline in profit margins. Since 2023, the price war in the automotive industry has spread from the new energy sector to the fuel vehicle market, forming a competitive red ocean of all categories and prices. Although the intensity of the price war has weakened to some extent in 2025 with the continuous promotion of the national anti internal competition work, and the promotion effect on improving industry profits has been reflected, it still needs to be continuously adjusted.

The dual impact of macroeconomic and policy environment further restricts the room for profit improvement. From a macro perspective, the decline in PPI has put pressure on the pricing of automotive products, making it difficult for companies to transfer cost pressures through price increases. From a policy perspective, although policies such as subsidies and replacement updates for new energy vehicles have effectively boosted sales, the expected policy rollback has intensified short-term competition pressure due to the rush to install new vehicles by enterprises. Although the anti involution policy has shown results in upstream industries such as steel, its transmission in the automotive end market still needs time. In addition, the imbalance between the development of fuel vehicles and new energy vehicles has become prominent, and the decline in profits of fuel vehicles has not been fully offset by the growth of new energy vehicles. The painful period in the process of oil electricity transformation is still ongoing.

Looking ahead, the improvement of profit margins in the automotive industry still faces many challenges. The continuous increase in the penetration rate of new energy vehicles brings long-term opportunities to the industry, but the short-term competitive inertia of price for quantity is difficult to quickly reverse; The alleviation of upstream cost pressure requires the collaborative efforts of the industrial chain, and the restructuring of profit distribution pattern is a long-term process.

Cui Dongshu frankly stated that based on the downward trend of profit margins in previous years, the recent decline in profits in the automotive industry is still significant. Due to the obvious price advantage of new energy under policy support, the profit pressure on mainstream car companies will continue to increase sharply.

However, with the deepening of the national anti involution work, the implementation of policies such as equal rights for oil and electricity, and the continuous efforts of enterprises in technological innovation and cost control, the industry is still expected to gradually get rid of the dilemma of bloated scale and meager profits, and achieve a steady recovery in profit margins.